Over a billion dollars liquidated in crypto’s worst day since FTX

Key Takeaways

- Last week saw crypto suffered its worst 24 hours since FTX as over one billion dollars in derivatives were liquidated on Thursday

- Derivative volume outstrips the extremely low spot volume, with cascading liquidations having the potential to exacerbate price moves

- Volatility was sparked by sell-off in the bond market

- Developments re-affirm how vulnerable Bitcoin is in the short-term to the highly unusual macro climate

Following an extended period of rest in the crypto markets, the beast re-awakened last week. Crypto markets plummeted late Thursday and early Friday, led as always by Bitcoin. The world’s largest cryptocurrency shed 7% in what amounted to the largest one-day drop since the spectacular collapse of FTX last November.

The year 2023 has been characterised thus far by the unusual fact that crypto’s rise has been slow and steady. Aside from a jump in March amid the regional bank crisis, Bitcoin has been perceptively devoid of the usual spikes and freefalls.

The Bitcoin price displays this clearly in the next chart, as well as Friday’s trip south.

Digging further into last week’s price drop shows that, remarkably, Bitcoin fell 8% in just ten minutes from 9:35 PM GMT on Thursday evening. Looking at data from Coinglass, this contributed to a surge of liquidations. All in all, over one billion dollars was liquidated in what amounted to the biggest day of liquidations since the FTX demise (anytime the phrase “since FTX” is used in crypto, it rarely spells good news).

The flood of liquidations highlights how much greater the volume was in derivatives markets than spot, with the latter remaining extremely thin. Order books have been perceptibly shallow ever since Alameda evaporated amid the FTX debacle (liquidity was thin even before then).

What caused the sell off?

The underlying cause of the volatility was a sell-off in the bond market, with yields spiking to multi-year highs. Yields on long-term US government debt neared their highest level since 2007, UK 10-year gilts rose to their highest yield since 2008, and Germany’s 10-year bund reached its highest yield since 2011.

Higher yields spell trouble for risk assets, as we are well aware by now, with Bitcoin sent tumbling amid the tightening monetary environment last year. The recent move was borne out of investors betting that high interest rates will persist for longer than previously anticipated, or further hikes may not be as improbable as previously expected.

The inverse relationship between Bitcoin and yields has been strong, demonstrated in the below chart. Hence, Bitcoin’s drop is not surprising in the context of the developments in the bond market last week.

The sell-off reaffirms how vulnerable Bitcoin is to a macro situation that continues to perplex – high but falling inflation, while high interest rates contrast with record-low unemployment and relatively resilient economic data.

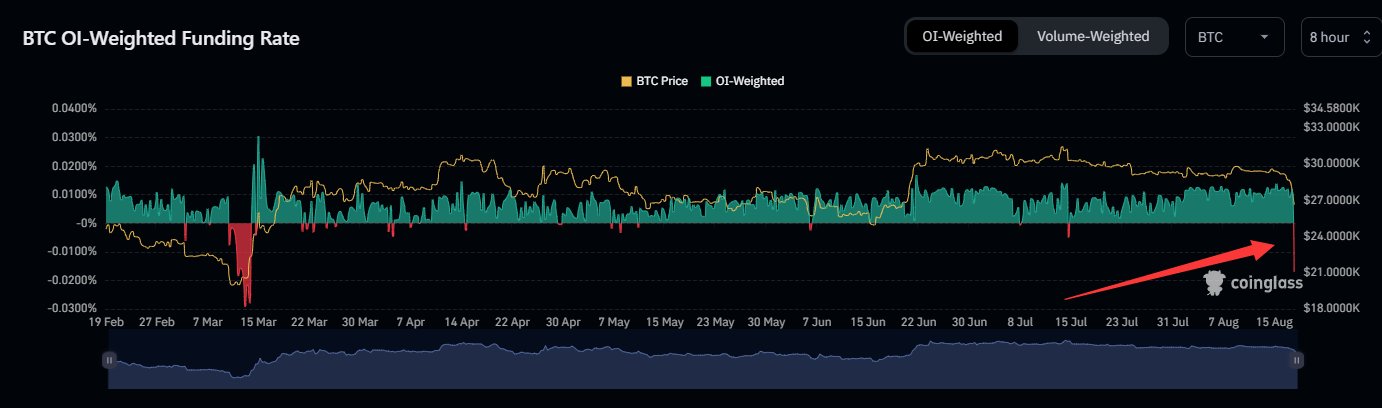

Getting back to the derivatives market, the shift was further evident by looking at funding rates, with the Bitcoin OI-weighted funding rate dipping below -0.01% for the first time since March.

Finally, negative funding rates and freefaling open interest returned. It took a while, but volatility has returned.

What next for crypto?

What this spells going forward is up for debate. Some analysts affirm this is a mere blip, a drop sparked by complacent overleverage following a period of calm that felt like forever. A slight increase in hawkish sentiment going forward won’t ultimately change much, they argue, for an economy which seems increasingly ambitious about achieving a soft landing.

On the other hand, some fear there could be a return to 2022-like conditions. While that may seem extreme, there is every change there is a recalibration away from the borderline-celebratory stance that interest rate hikes were complete and the soft landing was already guaranteed.

If that were the case, this could mark the end of the bear market rally for crypto. Few assets are as sensitive to global liquidity as Bitcoin is, meaning a reversion towards the tightening seen last year would undoubtedly spell red candles on price charts.

This would be getting ahead of oneself, however. The macro climate remains largely unprecedented and very challenging to predict. Even the Federal Reserve’s language betrays this, with some notable see-sawing in recent meetings.

Last Wednesday, meeting minutes said that there are “significant upside risks to inflation, which could require further tightening of monetary policy”. Going back to the meeting in July, minutes say that the Fed believed inflation was falling and risks “titled to the downside”, with Jerome Powell asserting that “given the resilience of the economy recently, (the Fed is) no longer forecasting a recession”.

While these are not necessarily conflicting – one can have inflation and tightening without a recession, it is just quite difficult (but where we have been living for the last eighteen months) – it does highlight how uncertain the whole climate is.

Bitcoin is again caught in the crossfire, a risk asset subject to the whims of the wider market as it grapples with this fast-changing environment.